In Ghana, insurance penetration remains relatively low. Despite the growth of the industry, a significant part of the population does not have access to insurance products.

This gap provides an opportunity for embedded finance to play a transformative role in enhancing insurance penetration.

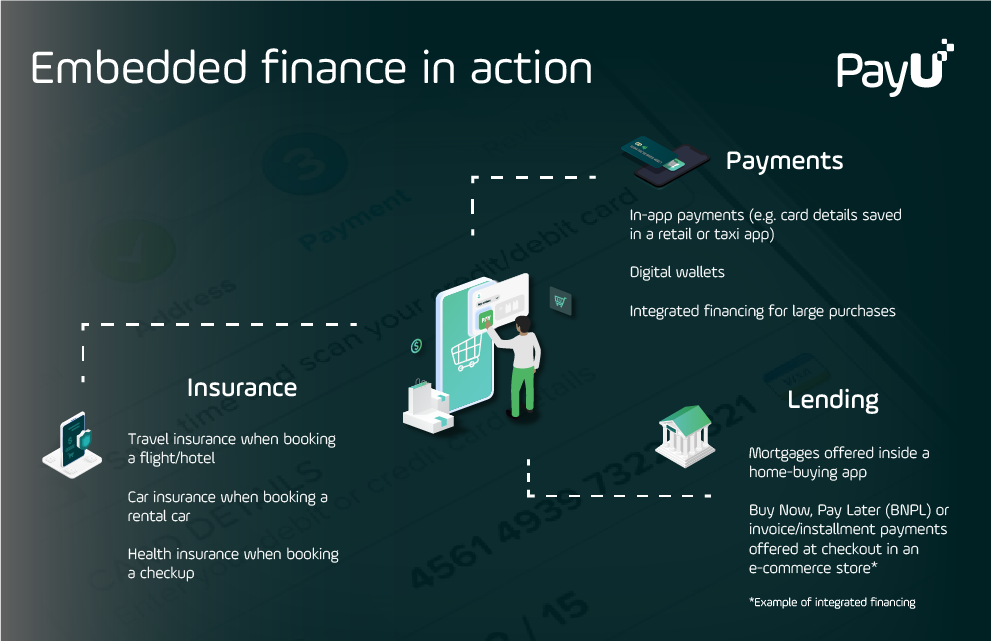

What is Embedded Finance?

Built-in financing refers to the integration of financial services into non-financial business platforms, allowing consumers to seamlessly access those services during their regular interactions with the business.

This approach can be particularly effective in markets such as Ghana, where traditional banking and insurance services may not reach the entire population.

Possibility of integrated financing

The potential of embedded finance in Ghana’s insurance sector is multi-faceted. First, it can increase accessibility. By integrating insurance offers into widely used services, such as e.g mobile platforms or retail storesinsurance is becoming more affordable to the average Ghanaian.

This ease of access is vital in a country where, according to a 2021 UNDP survey, about 70% of Ghanaians do not have insurance.

Second, embedded financing can enhance understanding and confidence in insurance products. Often, the lack of insurance uptake is due to a lack of understanding or mistrust of the products. By integrating insurance into everyday services and products, companies can leverage existing relationships with their customers to educate and build trust.

In addition, embedded financing can lead to the development of more personalized insurance products. With access to customer data, companies can design insurance products that better meet the specific needs of different consumer segments. This customization can lead to higher uptake and satisfaction rates.

politicians

The National Insurance Commission (NIC) of Ghana has recognized the need for innovation in the sector. The Insurance Act of 2021, for example, it introduced a special license for companies with new or innovative products or services, with the aim of modernizing the industry and increasing penetration.

Challenges

However, implementing embedded finance is not without its challenges. It requires strong regulatory frameworks to ensure consumer protection and data privacy. In addition, there needs to be a concerted effort from both the financial and non-financial sectors to work together and drive the adoption of integrated finance.

In conclusion, embedded financing holds the promise of significantly increasing insurance penetration in Ghana. By making insurance more accessible, understandable and tailored to the needs of consumers, it can play a critical role in the financial inclusion of Ghanaians.

As the country continues to navigate the digital transformation of its financial services, embedded finance could be the key to unlocking the insurance sector’s full potential.

Follow us on our WhatsApp channel, Twitterand Instagramand subscribe to our weekly newsletter to make sure you don’t miss any news.

Related