Presentation by Ethel Cofie, CEO of EDEL Technology

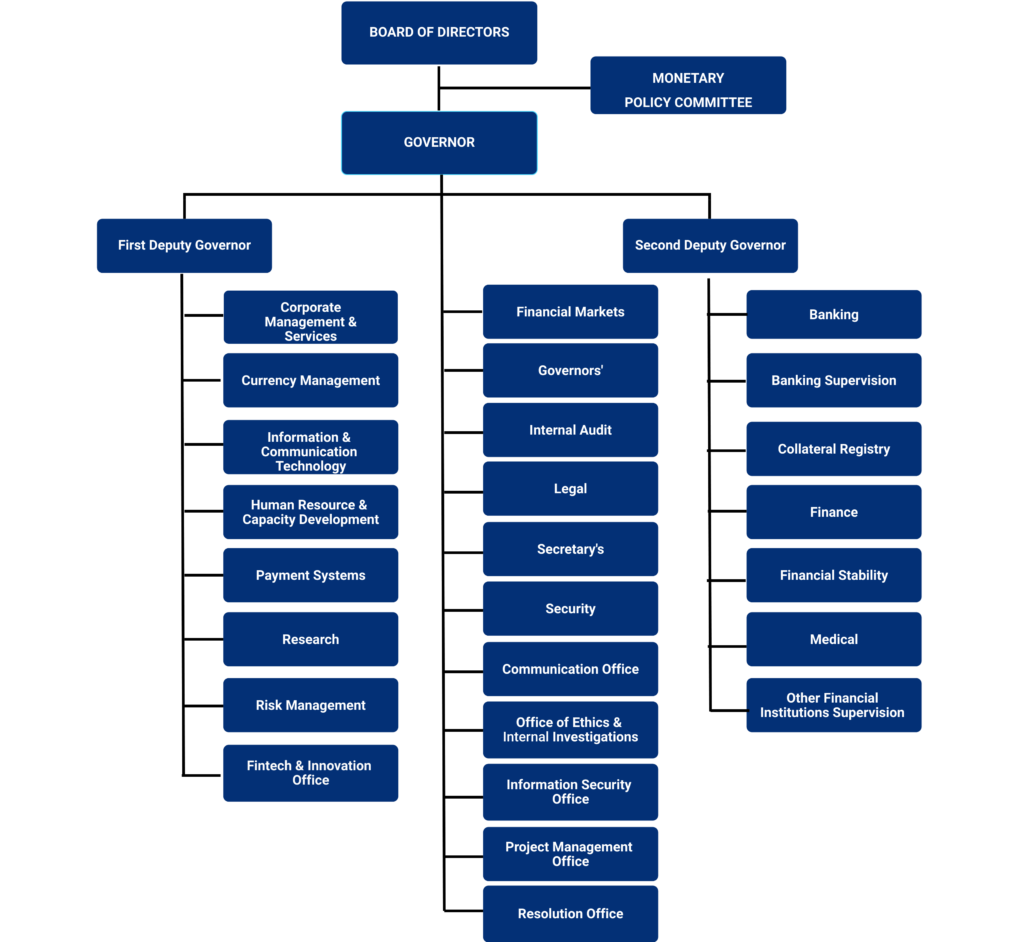

In an era characterized by rapid technological development, the financial sector is at the forefront of digital transformation. The Bank of Ghana, under its current governance structure set by the Act of 2002 (Act 612) and its Amendments, which allows only two lieutenantsfaces significant limitations in its ability to integrate and oversee developments in fintech and digital banking.

This article advocates an amendment to include a third deputy governor with a specialized focus technology, innovation and fintech.

This role is vital not only in moving Ghana towards a digital economy, but also in enhancing financial inclusion, security and international competitiveness.

The Impact of Fintech on the Ghanaian Economy: A Data-Driven Analysis

Enhanced financial inclusion

Fintech, particularly through mobile money services, has greatly expanded financial access in Ghana. According to the GSMA, Ghana is one of the fastest growing mobile money markets in Africa, with the volume of mobile money transactions increasing from 982 million in 2017 to over 2 billion transactions in 2020.

This growth has dramatically boosted financial inclusion, bringing financial services to about 58% of Ghana’s adult population as reported by the World Bank in 2021, up from 41% in 2015.

Strengthening Economic Development

The integration of fintech has made financial transactions faster, cheaper and more accessible, which has boosted economic activity. ONE study by the Brookings Institution stressed that mobile money services in Ghana could reduce transactions cost up to 75%.

In addition, the Bank of Ghana reported that mobile money transactions contributed significantly to GDP, with the estimated value of transactions reaching GHC 569 billion (approx. USD 98 billion) in 2020, showcasing the economic scale and impact of fintech innovations.

Creation of new jobs and industries

The fintech sector has become a major source of employment in Ghana. According to Ghana Chamber of Telecommunicationsonly the mobile money sector is of immediate concern over 200,000 agents nationwide.

In addition, the rise of investment-backed fintech startups surpassing $100 million in 2019according to the Disrupt Africa Funding Report, has further expanded employment opportunities in technology-focused roles and support services.

Promotion of Innovation and Entrepreneurship

Fintech has catalyzed a broader wave of tech entrepreneurship in Ghana. Innovation hubs and incubators like MEST Ghana and Impact Hub Extreme have flourished, supported by both local and international investment.

These hubs encourage innovation not only in fintech but across many sectors, helping to nurture a new generation of entrepreneurs. The growing startup ecosystem is evidenced by the success of local startups such as Zeepay, a fintech company that recently raised $3 million in funding to expand its operations across Africa.

Government revenue and tax collection

Digital payment platforms have greatly improved the efficiency of tax and revenue collection systems in Ghana. The introduction of digital solutions has facilitated easier and faster payments of taxes and utility bills, leading to higher compliance rates.

According to the Ghana Revenue Authority, the integration of mobile money solutions into tax processes contributed to the increase in domestic tax revenue, which increased by 16.3% in reach 53 billion GHC (about 9 billion USD) in fiscal year 2020.

The limitations of the current structure of the Bank of Ghana

The current position of Chief Innovation Officer at the Bank of Ghana is an important step towards the adoption of technology in the financial systems. However, this role does not have a seat on the Board of Directors of the Bank of Ghana.

A deputy governor, by contrast, would have executive authority to influence broader monetary policies and integrate advanced technology strategies directly into the bank’s core operations at a strategic and operational level. This difference in scope and influence is critical to Strategic Oversight and Policy Development.

The Global Digital Shift: Why Ghana Can’t Afford to Delay

Around the world, central banks are redefining their structures by creating board-level or equivalent technology positions to better navigate the complexities of a digital economy. For example:

- The Bank of England employs a Chief Data Officer at a senior executive level to integrate technology and data analytics into financial stability strategies.

- The Monetary Authority of Singapore appointment of a Chief FinTech Officer underlines the importance of placing such roles within the top executive team to effectively promote national fintech initiatives.

- Federal Reserve Bank (USA) his appointment Director of Innovation Center (FedNow Service) meant that the Federal Reserve has been actively involved in technology through various initiatives, including the development of FedNow, a service aimed at modernizing the US payment system with real-time payment capabilities scheduled to launch in 2023.

Without a dedicated high-level leadership role focused on these areas, Ghana risks falling behind in both regional and global financial innovation, potentially missing out on the economic growth opportunities presented by the digital age.

This role will catalyze much-needed reforms in the financial sector, reduce bureaucratic inertia and ensure that initiatives such as the national digital identity scheme and mobile money taxation reforms are implemented effectively and efficiently.

Strategic Benefits of Third Deputy Commander

Enhanced regulatory oversight: A tech-focused lieutenant governor can lead the way in developing regulations that not only encourage innovation but also ensure stability and security in the digital financial sector. This role could directly address emerging challenges, such as cyber threats, which are becoming increasingly important as financial transactions are digitized.

Leadership in Financial Technology: With initiatives leading around blockchain, mobile money interoperability and digital currencies, Ghana could set a regional benchmark in fintech

Promoting financial inclusion: With a strategic focus on leveraging technology to reach underserved populations, a third deputy governor could bolster efforts to integrate larger segments of the Ghanaian population into the formal economy. This is particularly important considering that from 2021, only 58% of Ghanaian adults have a bank account, according to World Bank data.

Overcoming barriers to innovation

The addition of a dedicated deputy governor will align the Bank of Ghana’s leadership with the country’s broader goals of becoming an innovation hub in West Africa.

This role will catalyze much-needed reforms in the financial sector, reduce bureaucratic inertia and ensure that initiatives such as the national digital identity scheme and mobile money taxation reforms are implemented effectively and efficiently.

Conclusion and call to action

Amending the Bank of Ghana Act to include a third deputy governor focused on technology and innovation is not just an organizational change but a strategic imperative. This amendment will enable Ghana to fully leverage the potential of fintech for economic growth, address emerging risks associated with digital finance and position Ghana as a leader in the digital economy of the future.

This is reposted from Ethel Cofie’s blog